CME Group plans to make its cryptocurrency futures and options trade around the clock beginning May 29, a product line that posted $3 trillion in notional volume in 2025 and is running 46% above that pace year-to-date.

ICE’s New York Stock Exchange is developing a tokenized securities platform built for 24/7 operations, instant settlement, dollar-sized orders, and stablecoin-based funding, pending regulatory approvals.

Both exchange operators have directed capital and infrastructure toward the same always-open structure pioneered by crypto-native venues.

Bloomberg reported on May 15 that the same two exchange giants are pressing US officials to rein in Hyperliquid, the offshore crypto venue that built the model before either incumbent filed.

According to people familiar with the discussions, CME and ICE alleged that Hyperliquid’s anonymous trading environment could distort global oil prices, facilitate market manipulation, and enable state actors to circumvent sanctions enforcement.

Bloomberg had separately reported in March that a Hyperliquid perpetual contract tracking WTI crude generated more than $1.2 billion in 24-hour volume during a traditional-market oil spike, briefly becoming the platform’s second-most-traded market.

The fight that CME and ICE are allegedly taking to Washington is over who gets to run continuous markets when oil is on the table, and if policymakers will treat it as a market-integrity question or a competitive one.

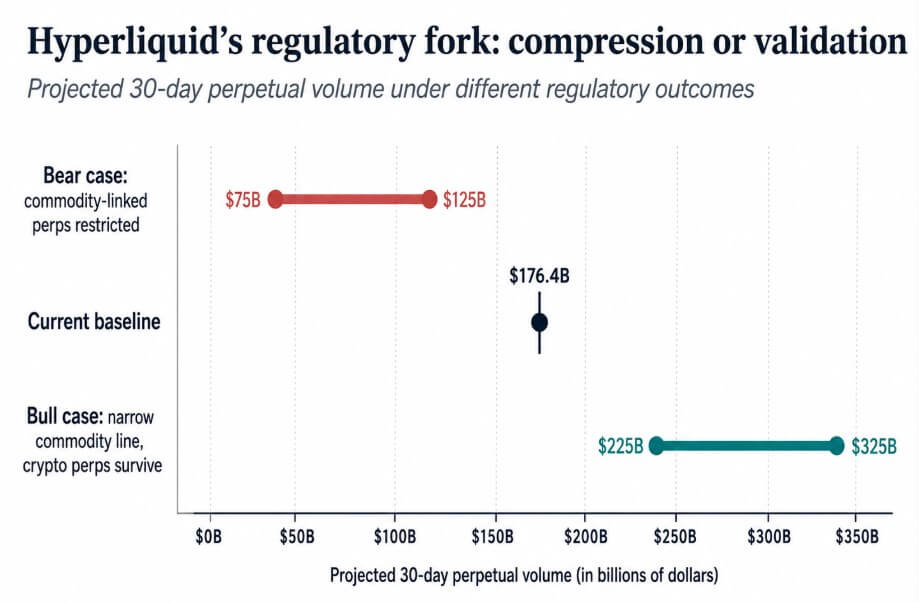

Venue / operator24/7 market moveWhy it mattersCME GroupCrypto futures/options go 24/7 on May 29; $3T notional volume in 2025; +46% YoY YTD paceIncumbent validation of always-open crypto marketsICE / NYSETokenized securities platform for 24/7 operations, instant settlement, dollar-sized orders, stablecoin fundingWall Street adopting crypto-style market structureHyperliquidAlready live; $176.4B 30-day perp volume; $7.9B 24h volume; $9.3B open interestCrypto-native venue proved the model before incumbents scaled it

DeFiLlama lists Hyperliquid with approximately $176.4 billion in 30-day perpetual volume, $7.9 billion in 24-hour perpetual volume, and $9.3 billion in open interest, annualizing to roughly $2.15 trillion.

Hyperliquid accounts for 31.7% of 30-day on-chain perp DEX volume but holds 58.5% of perp DEX open interest, carrying nearly 60% of position-bearing liquidity in the sector while accounting for less than 33% of its trading volume.

The structure runs as a fully on-chain order book, where every trade and liquidation settles with one-block finality on its own L1, and its HIP-3 framework lets developers deploy permissionless perpetual markets with customizable oracles, leverage limits, and settlement parameters.

The market function this architecture delivers, consisting of always-open, leveraged, electronic exposure to major assets, runs on fully on-chain infrastructure, with pseudonymous participants and permissionless market creation.

The market integrity argument

CFTC-regulated designated contract markets must maintain automated surveillance systems, real-time monitoring, audit-trail data capable of reconstructing every trade, and formal mechanisms to investigate and discipline misconduct.

The CFTC was exercising exactly those detection capabilities when it examined oil futures trades placed on CME and ICE platforms before major President Donald Trump administration Iran-policy announcements.

Reports found an approximately $950 million bet on falling oil prices placed hours before a US-Iran ceasefire announcement, and a roughly $500 million oil-futures position established shortly before a Mar. 23 policy announcement.

Representative Ritchie Torres separately called for the SEC and CFTC to investigate the $950 million trade, saying its timing raised questions about potential insider trading and market integrity.

The CFTC ordered JPMorgan to pay $920.2 million in 2020 for spoofing and manipulation in precious metals and Treasury futures, then the largest monetary relief the agency had ever imposed in a spoofing case.

Enforcement actions against TotalEnergies Trading, Trafigura, Glencore, Vitol, and BP in commodity markets over the past decade show the same pattern, where misconduct reached material scale before enforcement intervened, with regulation providing the tools to detect and punish it only when the damage was done.

The enforcement record shows that well-timed or suspicious trades can reach material scale inside regulated perimeters before anyone intervenes, as the most recent Iran-linked oil-price moves, those trades were executed on the CME and ICE platforms.

Case / eventVenue or market contextAmount / scaleArticle takeawayIran-linked oil trade before ceasefireCME / ICE platforms, per Reuters~$950MSuspicious timing can occur inside regulated venuesOil-futures position before Mar. 23 announcementCME / ICE platforms, per Reuters~$500MSurveillance may detect trades after the factJPMorgan spoofing/manipulation casePrecious metals and Treasury futures$920.2M penaltyRegulated markets still require enforcementCommodity-market cases involving TotalEnergies, Trafigura, Glencore, Vitol, BPOil, gas, and commodity marketsMultiple enforcement actionsMarket integrity failures are not unique to crypto

Outcomes if the report is accepted

If regulators accept CME and ICE’s reported framing, the enforcement focus will land on Hyperliquid’s commodity-linked markets.

Oil-linked perps face access restrictions, oracle disclosure requirements, or geofencing by front-end providers, while crypto perpetuals fall into a separate regulatory bucket.

Under that outcome, Hyperliquid’s 30-day perp volume compresses to a range of $75 billion to $125 billion, open interest contracts, and institutional BTC and ETH flows migrate toward CME’s regulated 24/7 futures.

If Washington draws a narrow line around commodity-linked perps and leaves crypto-native markets alone, or if the CFTC’s examination of Iran-linked oil trades on incumbent platforms undermines the case that offshore venues are uniquely dangerous, Hyperliquid retains its dominant position in on-chain perpetuals.

High oil volatility sustains demand for always-open exposure, the incumbent lobbying campaign validates the platform’s market position among existing users, and 30-day volume expands toward a range of $225 billion to $325 billion.

The crypto-native market structure remains competitive in speed and composability compared to anything regulated venues can build within compliance perimeters.

The US perpetual futures stay in a regulatory gray area, with most activity concentrated on offshore venues. A CFTC now examining suspicious oil trades on its own licensed platforms enters any offshore enforcement action with a narrower rhetorical runway.

CME and ICE are building continuous markets, and Hyperliquid has already shown how strong the demand for them is. The incumbents are taking a jurisdictional fight to Washington over who controls markets that are always open when the underlying asset is oil.

Whether regulators treat that as a genuine market-integrity concern or as competitive repositioning by incumbents who arrived late to the model will determine which institutions control default-trading infrastructure in the next decade.